The Angel Capital Deployment Gap

Record numbers of angel investors. A decade low in capital deployed. What is driving the divergence and what it means for founders.

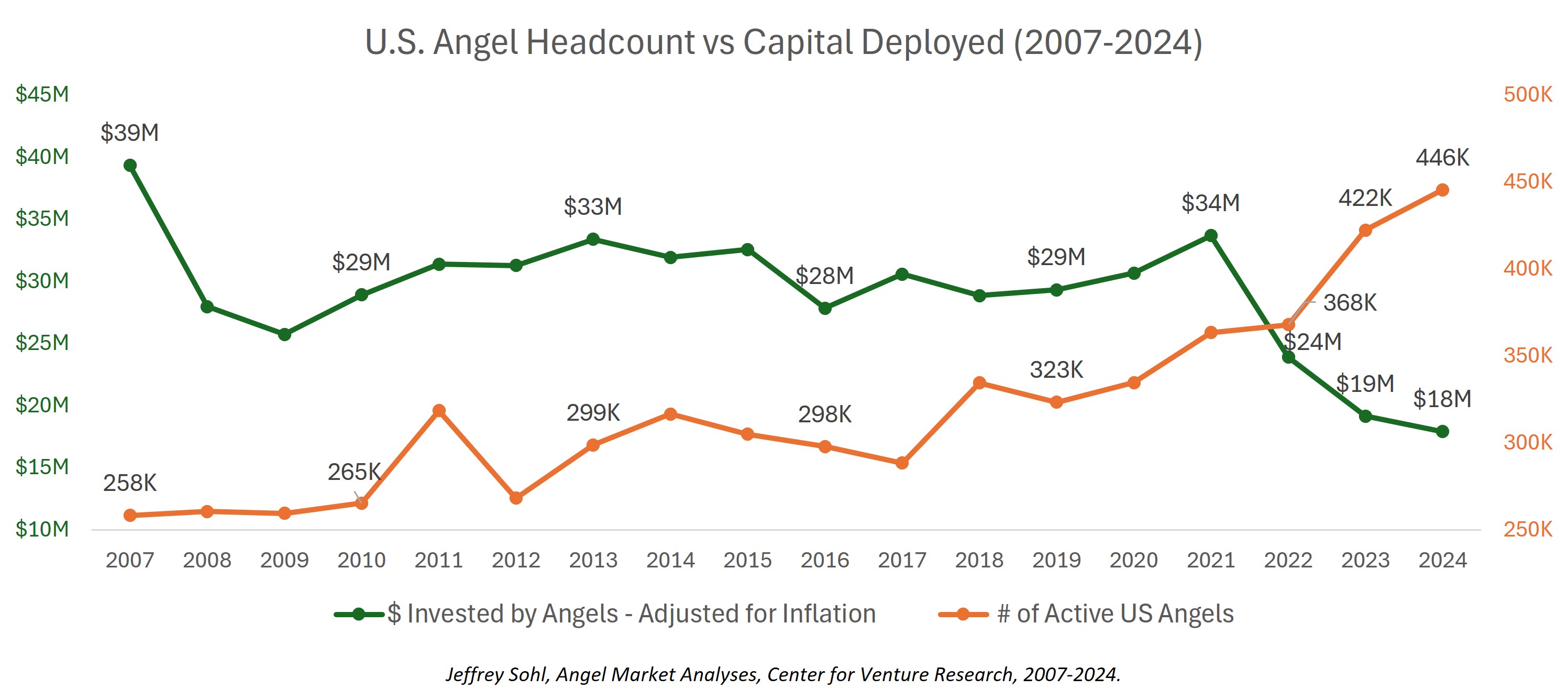

At first glance, the angel investing ecosystem looks healthier than ever. The number of active U.S. angel investors has grown from roughly 200,000 in 2002 to over 445,000 in 2024, more than doubling in two decades.¹ Yet beneath that headline figure lies a troubling paradox: as the ranks of angels have swelled, the total capital they deploy into startups has been quietly collapsing.

In 2021, angel investors collectively deployed $29.1 billion ($32.3 billion in today's dollars) in total angel investments. By 2024, that figure had fallen to $17.9 billion, a decline of more than 38% in just three years.¹ Zoom out further and the picture is even starker. Angels invested $30 billion ($53 billion in today's dollars) back in 2001. More than twenty years later, with more than twice as many investors in the market, total deployment is actually lower in nominal terms and sits at roughly one-third of the 2001 figure when adjusted for inflation.¹

A Market Expanding in Bodies, Contracting in Dollars

The divergence between investor count and capital deployed is the defining tension in today's angel market. As the chart below shows, these two lines have been moving in opposite directions since 2021, angel headcount climbing steadily while total investment has fallen sharply.

Between 2022 and 2024 alone, the number of active angels climbed from approximately 368,000 to 445,000, a jump of more than 21%. Over that same window, total dollars invested fell from $22.3 billion ($23.0 billion in today's dollars) to $17.9 billion.¹ The bars in the chart make clear this is not a gradual drift. It is a sharp inflection following the 2021 peak.

The simplest way to frame what is happening: total capital per angel has declined significantly. Three questions the data raises but cannot answer on its own:

Are angels writing fewer checks per year, becoming more selective as the environment gets tougher?

Are they committing less capital per deal, hedging their bets in an uncertain market?

Or is some portion of the registered angel population no longer actively deploying at all, inflating the headcount while the true base of engaged investors quietly shrinks?

The answer is likely some combination of all three, and that ambiguity matters. More angels in the room does not necessarily translate to more money in the bank.

What is driving the contraction? Several well-documented forces are at work:

A stock market offering hard-to-beat returns. The S&P 500 posted back-to-back gains exceeding 20% in 2023 and 2024, the first time that has happened since 1998.² For a potential angel weighing the prospect of tying up capital in an illiquid startup for seven to ten years, liquid equity markets delivering outsized returns represent a genuine alternative. Why take on the risks of early-stage investing when a passive index fund is outpacing historical averages?

A drought of exits limiting capital recycling. When angels cannot get liquidity from prior investments, they have less fresh capital to redeploy into new ones. The Angel Capital Association has documented a significant dry spell in exits since 2021, with both the number of exits and the average multiples realized declining dramatically, reducing the capital available for reinvestment into new deals.³

A valuation mismatch squeezing deal economics. At the same time, pre-seed and seed-stage valuations have surged. Pre-seed valuations doubled to roughly $10 million in 2024 after holding steady near $4–5 million since 2021, with seed-stage valuations reaching the same level, while later-stage exit multiples declined sharply over the same period.⁴ Angels are being asked to pay more for earlier-stage companies at a moment when the returns at the end of the pipeline have compressed. That mismatch is keeping capital on the sidelines.

Declining deal flow quality. ACA data shows that early-stage funding by angel groups dropped 33% in 2023 compared to 2022, with average funding per deal falling 15%, on top of a 27% drop the year prior.⁵ Fewer compelling deals reaching angels means fewer dollars going out the door.

A Bright Spot: Seed and Startup-Stage Deals Are Surging

Not every trend in the data tells a story of retreat. One genuinely encouraging signal is the growing share of angel dollars flowing into the earliest-stage companies, the seed and startup stage.

In 2024, 59% of all angel investment activity was directed toward seed and startup-stage companies, up dramatically from 41% in 2023 and the highest level in the dataset going back to 2001.¹ This is a meaningful shift. It suggests that even as total capital contracts, angels are increasingly concentrating what they do deploy at the moment founders need it most, before they have revenue, customers, or institutional backing.

This was not always the case. Through much of the 2000s and 2010s, angel capital was more evenly distributed across stages, including expansion-stage companies further along in their development. In 2014, for instance, only 25% of angel activity targeted seed and startup companies, with nearly half going to companies already further along.¹ The trend since then has been a consistent reorientation toward earlier-stage bets.

This matters for the startup ecosystem. Seed and startup-stage capital is often the most catalytic, funding the experiments that determine whether a company is worth building at all. Angels stepping into this gap, at a stage where institutional venture capital has historically been reluctant to venture, play an outsized role in determining which ideas get a real chance.

What This Means for Founders

The data paints a nuanced picture for entrepreneurs seeking angel capital. On one hand, there are more potential investors to approach than at any point in history, and a higher proportion of them are willing to back ideas at the earliest, riskiest stages. On the other hand, the total pool of available capital has shrunk significantly, meaning competition for each dollar is more intense even as the number of angels grows.

Founders raising pre-seed or seed rounds may find a receptive audience, but should expect that individual check sizes are smaller, and that assembling a meaningful round will likely require more investors at the table than it would have five years ago.

For the angel investor community itself, the trends raise a longer-term question: as more people enter the asset class and average capital per investor declines, does the quality of angel engagement, the mentorship, networks, and operational support that distinguish great angels from passive check-writers, inevitably dilute as well?

Looking Ahead: 2025 and the AI Question

The dataset ends in 2024, just as the AI investment boom was beginning to reshape the broader startup funding landscape. It would be tempting to assume that AI's rise reversed the contraction visible in the chart above. The early evidence suggests otherwise.

The structural headwinds that drove the post-2021 decline did not fully resolve in 2025. Major liquidity events remained infrequent, limiting the recycling of exit proceeds back into new angel bets. Public equities continued offering competitive returns with far greater liquidity. The Angel Capital Association's own 2025 report noted that overall deal volume softened further and exits slowed, even as angels demonstrated resilience in maintaining early-stage commitments.⁶

AI complicated the picture rather than clarifying it. Technology-led industries pulled an estimated 68% of all angel investment dollars in 2025, concentrating what was already a shrinking pool into a narrower set of bets.⁷ For founders operating outside those favored categories, the funding environment grew more challenging still.

Perhaps most telling is the structural mismatch between where AI deals happen and where angels typically play. The rounds that matter most in AI, Series A and beyond, are institutional territory. The best AI startups are racing past the seed stage almost immediately, often bypassing the angel-led rounds where individual investors have historically added the most value. Rather than expanding the opportunity set for angels, the AI boom may actually be compressing it.

The more durable shift in 2025 was behavioral. Angels became more selective, prioritizing traction, capital efficiency, and defensible business models over vision alone. Fewer checks, written with more conviction. Whether that discipline translates into better outcomes for the asset class, or simply fewer founders getting a shot, remains to be seen.

Conclusion

The angel market is not in crisis, but it is under real pressure. Capital has contracted sharply even as the investor base has grown, and the structural forces behind that gap have not yet resolved. The encouraging sign is that what capital remains is flowing earlier than ever, to the seed and startup-stage companies that need it most. Whether a leaner, more selective angel market ultimately strengthens the startup ecosystem or simply narrows who gets a shot at building something is what the next few years of data will reveal.

Sources

UNH Center for Venture Research, Peter T. Paul College of Business and Economics. Angel Market Analysis Reports, 2001-2024.

Statista. "S&P 500 Clocks Back-to-Back 20% Gains for First Time Since 1998." January 2025.

Angel Capital Association. "Where Have All the Exits Gone?" November 2024.

Angel Capital Association. "The Early Stage Valuation Disconnect." August 2025.

Angel Capital Association. Angel Funders Report 2024.

Angel Capital Association. Angel Funders Report 2025. August 2025.

K4 Northwest. "Early-Stage Investing in 2025: The Data, the Shifts, and the Signals You Can't Ignore." November 2025.